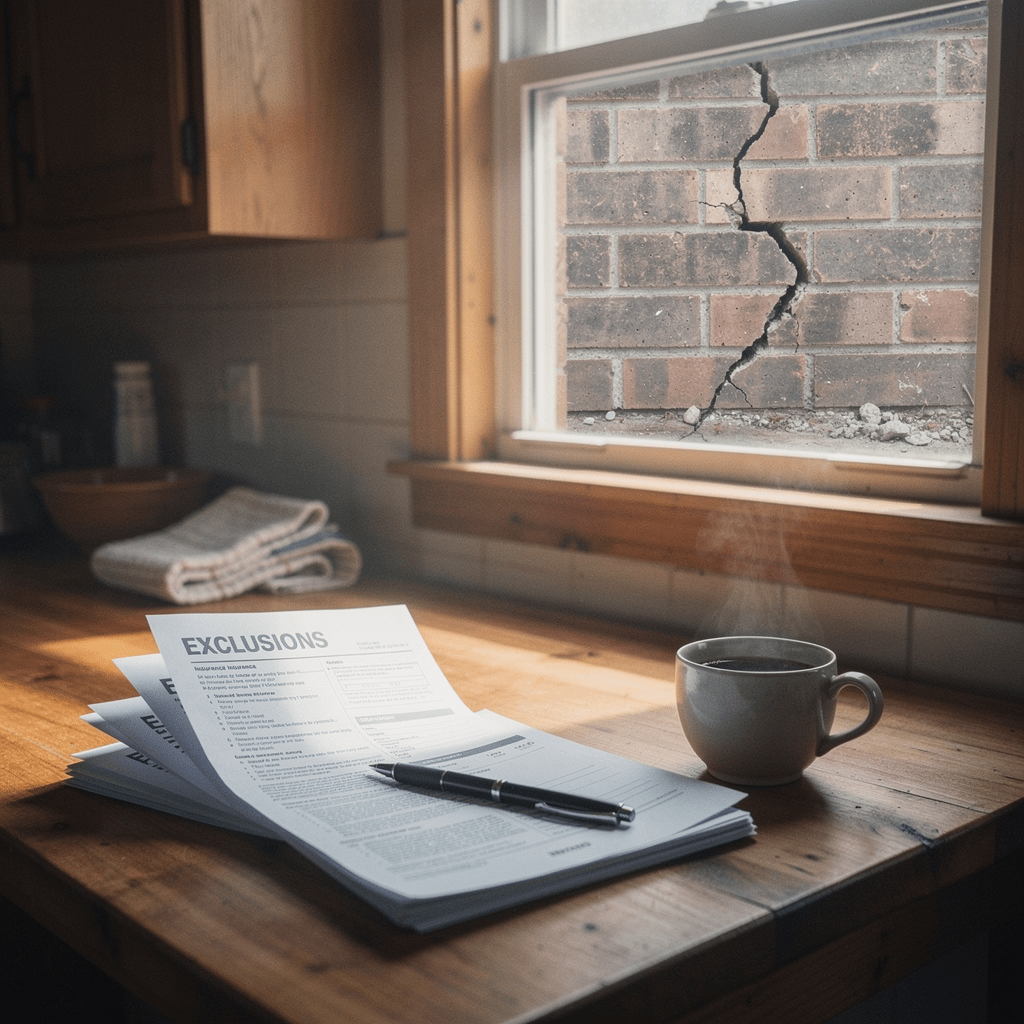

It’s one of the first things North Texas homeowners ask when they realize their foundation has a problem: “Will my homeowners insurance cover this?”

It’s an understandable question. Foundation repair costs can range from a few thousand dollars to well over $20,000. The prospect of insurance covering even part of that is enormously appealing. And because the answer feels like it should be straightforward — you have insurance, your home has damage — many homeowners are genuinely shocked when they discover the reality.

The short version: in most cases, standard homeowners insurance does not cover foundation repair in Texas. But the full answer is more nuanced than that, and understanding the exceptions — and the specific scenarios where coverage does apply — can make a meaningful difference in how you approach both the repair and the claim process.

This guide explains exactly how Texas homeowners insurance treats foundation damage, when coverage does and doesn’t apply, what you can do to protect yourself financially, and why getting a professional engineering assessment is critical before you file any claim.

How Texas Homeowners Insurance Treats Foundation Damage

Standard homeowners insurance policies in Texas are written on a named-peril or open-peril basis, meaning they cover damage caused by specific events (or all events not explicitly excluded, depending on policy type). Foundation damage falls into a gray area because the cause of the damage — not the damage itself — determines whether coverage applies.

Texas homeowners policies are typically issued using the Texas Department of Insurance’s standard policy forms. Under these forms, foundation damage is generally excluded when caused by:

- Earth movement — including soil expansion and contraction (the primary cause of foundation damage in North Texas)

- Settlement or shrinkage — the gradual movement of soil and structure over time

- Hydrostatic pressure — water pressure from saturated soil pushing against a foundation

- Tree root intrusion — roots disrupting soil stability or penetrating structural components

- Poor construction or design defects — inadequate original engineering

These exclusions cover the vast majority of foundation problems in Tarrant, Wise, and Parker Counties — because the overwhelming cause of foundation movement in this region is expansive clay soil behavior, which falls squarely under the earth movement exclusion.

When Does Homeowners Insurance Cover Foundation Damage?

There are specific, defined scenarios where homeowners insurance may cover foundation-related damage. Understanding them is worth the effort.

Sudden and Accidental Water Damage

If a pipe bursts inside your home and water floods the subfloor or undermines the foundation, the resulting damage may be covered under your dwelling coverage. The key qualifier is sudden and accidental — chronic seepage, gradual leaks, or long-running slab leaks are typically excluded.

However, if a slab leak has been slowly saturating the soil beneath your foundation for months or years, you are almost certainly outside the coverage window regardless of when you discovered it. Insurers look at the duration of the damage, not just the discovery date.

Slab Leaks — A Specific Texas Issue

Slab leaks — broken or leaking pipes embedded within or beneath a concrete slab — are extremely common in North Texas homes. Some Texas homeowners policies include coverage for the cost of accessing the leak (cutting through concrete, tunneling, excavation) even if they don’t cover the resulting foundation repair itself.

This distinction matters practically: if your policy covers access costs for plumbing repair but not the foundation damage the leak caused, you may still receive partial reimbursement. Read your policy carefully on this point, or ask your agent directly.

Fire, Explosion, or Vehicle Impact

Foundation damage caused by a fire, gas explosion, or a vehicle striking the structure would be covered under standard dwelling coverage as a sudden, accidental peril. These scenarios are rare but worth noting for completeness.

Collapse Coverage

Some policies include coverage for sudden structural collapse caused by specific named perils — including the weight of ice, snow, or sleet, or damage from insects and vermin. If pier and beam floor collapse results from termite damage that can be linked to a covered peril, there may be a claim pathway, though insurers scrutinize these closely.

The Flood Insurance Gap

Many North Texas homeowners experience significant foundation-related damage during major flooding events — heavy spring rains, creek overflow, prolonged soil saturation. Standard homeowners policies explicitly exclude flood damage. Flood coverage requires a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private flood insurer.

Even with flood insurance, coverage for foundation systems specifically can be limited. Flood policies typically cover the physical structure and its systems up to policy limits, but coverage calculations for foundation components vary based on policy type and damage assessment.

If you are in a designated flood zone in Tarrant, Wise, or Parker County, this gap is worth discussing with your insurance agent before a problem develops.

What About Home Warranties?

Home warranties — the annual service contract products sold by companies like American Home Shield, Choice Home Warranty, and First American — are separate from homeowners insurance. Most standard home warranties do not cover foundation structural repair. Some premium-tier home warranty add-ons cover plumbing systems, which could include slab leak access and pipe repair, but structural foundation work is almost universally outside the scope of these products.

Do not assume a home warranty covers foundation repair without reading the specific terms of your contract.

Why the Engineering Report Is Critical Before Filing Any Claim

If you believe your foundation damage may have an insurance-covered cause — a sudden pipe burst, documented flooding, a specific datable event — the single most important thing you can do before filing a claim is obtain a professional structural engineering report.

Here’s why this matters:

Insurance adjusters assess cause, not just damage. When an adjuster visits your home, they are evaluating whether the cause of the damage falls within a covered peril. Without a professional engineering report that documents the cause, timeline, and structural impact of the damage, you have no independent evidence to support your claim or contest a denial.

Engineering reports are your documentation. A licensed structural engineer’s report establishes a professional record of the damage that exists independent of the insurance company’s adjuster. If the insurer denies your claim and you choose to dispute it — through a public adjuster or legal process — the engineering report is your foundational evidence.

The order matters. Get the engineering report before repairs begin. Once the damage is repaired, documenting the original cause and severity becomes exponentially harder.

At Tri-County Foundation Repair, our process starts with exactly this: a $1,100 engineering inspection that produces a written report you own. If there is any possibility of an insurance claim, having that report in hand before you call your insurer puts you in the strongest possible position. Learn more about what that inspection covers in our detailed breakdown of what the $1,100 foundation inspection actually includes.

What to Do If Your Claim Is Denied

Foundation repair claim denials are common in Texas, but they are not always final. If your claim is denied, you have several options:

Request a written denial with the specific policy exclusions cited. You are entitled to a written explanation of any claim denial. Review the cited exclusions carefully against your actual policy language — adjusters sometimes apply exclusions incorrectly.

Hire a licensed public adjuster. Public adjusters are licensed professionals who represent policyholders — not insurance companies — in the claims process. They are paid on a percentage of the settled claim. For complex foundation claims, a public adjuster’s expertise in Texas policy language and damage documentation can be the difference between a denial and a partial settlement.

File a complaint with the Texas Department of Insurance. If you believe your claim was handled improperly — misrepresentation of policy terms, unreasonable delay, or bad faith denial — the TDI accepts complaints and investigates insurer conduct. Their website (tdi.texas.gov) provides a straightforward complaint process.

Consult a property insurance attorney. For larger claims, an attorney specializing in Texas property insurance disputes can evaluate whether a denied claim has grounds for appeal or litigation. Many operate on contingency for cases with clear merit.

Proactive Financial Planning for Foundation Repair

Because insurance coverage is limited for the most common causes of foundation damage in Texas, financial preparedness is the most reliable protection available to North Texas homeowners.

Home equity lines of credit (HELOCs). Many homeowners finance foundation repair through a HELOC, which uses home equity as collateral. Interest rates are typically lower than personal loans, and the credit line can be drawn as needed throughout the repair process.

Contractor financing. Some foundation repair contractors offer financing programs through third-party lenders. If you consider this option, review the interest rate and terms carefully — some contractor-referred financing products carry rates significantly above market.

Emergency funds. Financial advisors commonly recommend maintaining 1 to 3 percent of your home’s value in reserve for unexpected repair costs. For a $350,000 home, that’s $3,500 to $10,500 — enough to cover many foundational repairs at the lower end of the range.

Act early. This is the most financially impactful advice available. The cost difference between addressing foundation damage promptly versus delaying 12 months can be dramatic. We document this progression in specific detail in our post on how much waiting actually costs, month by month.

What North Texas Homeowners Should Do Right Now

Whether or not you have an active foundation problem, two proactive steps make a meaningful difference:

First, pull out your homeowners insurance policy — or call your agent — and ask specifically what your policy covers and excludes regarding foundation damage, earth movement, and slab leaks. Get a clear answer in writing. Many homeowners discover the gaps in their coverage only after a problem develops.

Second, if you’re already seeing warning signs — sticking doors, wall cracks, uneven floors — don’t wait for the damage to worsen. The wall cracks in your home may already be telling you something important, and the earlier a structural engineer evaluates the situation, the more options you have.

Call Tri-County Foundation Repair at (817) 406-4094 or contact us online. We serve Tarrant, Wise, and Parker Counties, and we’ll start with the engineering report that protects you — whether you’re filing an insurance claim, planning a repair, or just trying to understand what’s happening beneath your home.

Frequently Asked Questions: Homeowners Insurance and Foundation Repair in Texas

Does homeowners insurance cover foundation repair in Texas?

In most cases, no. Standard Texas homeowners insurance policies exclude foundation damage caused by earth movement, soil settlement, shrinkage, and expansive clay soil behavior — which are the primary causes of foundation problems in North Texas. Coverage may apply in specific circumstances, such as sudden pipe bursts that undermine the foundation or damage caused by named perils like fire or explosion. Because the cause of the damage determines coverage, not the damage itself, homeowners should review their specific policy language carefully and consult their agent.

Will insurance cover a slab leak that damaged my foundation?

It depends on your policy and the circumstances of the leak. Sudden and accidental pipe failures may trigger coverage for the cost of accessing and repairing the plumbing, and in some cases for resulting structural damage. However, long-running leaks discovered after extended periods of gradual seepage are typically excluded. Many Texas policies specifically cover access costs for plumbing repair beneath a slab — the excavation or tunneling needed to reach the pipe — even when the resulting foundation damage itself is not covered. Review your policy’s plumbing and water damage provisions carefully.

What type of foundation damage is covered by homeowners insurance?

Foundation damage caused by sudden, covered perils may be insured. This includes damage resulting from a sudden pipe burst, fire, explosion, or vehicle impact. Collapse caused by specific named perils — such as the weight of ice or damage from insects, in some policies — may also trigger coverage. The critical test is whether the damage resulted from a sudden, accidental, covered event rather than gradual deterioration, earth movement, or soil behavior.

Does flood insurance cover foundation repair?

Standard homeowners insurance explicitly excludes flood damage, which requires a separate flood insurance policy through the National Flood Insurance Program or a private insurer. Even with flood insurance, coverage for foundation structural components can be limited and varies by policy type. Homeowners in flood-prone areas of Tarrant, Wise, or Parker County should review their flood policy terms specifically as they relate to foundation systems.

Should I file a homeowners insurance claim for foundation damage?

Before filing any claim, obtain a professional structural engineering report that documents the cause, timeline, and extent of the damage. This report protects you regardless of outcome — it supports your claim if covered, and provides independent documentation if the claim is denied and you choose to dispute it. Filing a claim that is subsequently denied can affect your insurance record and future premiums in Texas, so understanding whether your specific damage has a plausible coverage pathway before filing is a worthwhile step.

How do I dispute a foundation repair insurance claim denial in Texas?

Start by requesting a written denial that cites the specific policy language and exclusions applied. Review that language against your actual policy document. If you believe the denial misapplies your policy terms, consider hiring a licensed public adjuster — who represents policyholders, not insurers — to re-evaluate the claim. For larger disputes, a Texas property insurance attorney can assess whether the denial has grounds for appeal or legal challenge. Complaints about insurer conduct can be filed with the Texas Department of Insurance at tdi.texas.gov.

Does a home warranty cover foundation repair?

Most standard home warranty products do not cover structural foundation repair. Some premium-tier home warranty plans cover plumbing systems, which may include the cost of accessing slab leaks but not the resulting foundation damage. Review your specific home warranty contract for foundation-related exclusions before assuming coverage exists.

How do most Texas homeowners pay for foundation repair?

Because insurance rarely covers the most common causes of foundation damage in Texas, homeowners typically pay out of pocket through one of several methods: personal savings or emergency reserves, home equity lines of credit (HELOCs), contractor-referred financing programs, or personal loans. Financial advisors generally recommend maintaining reserves equal to 1 to 3 percent of your home’s value for unexpected repair costs. Acting early — before damage escalates — is the most effective way to keep foundation repair costs within manageable ranges.